SEIS Advance Assurance,

FoodTech venture.

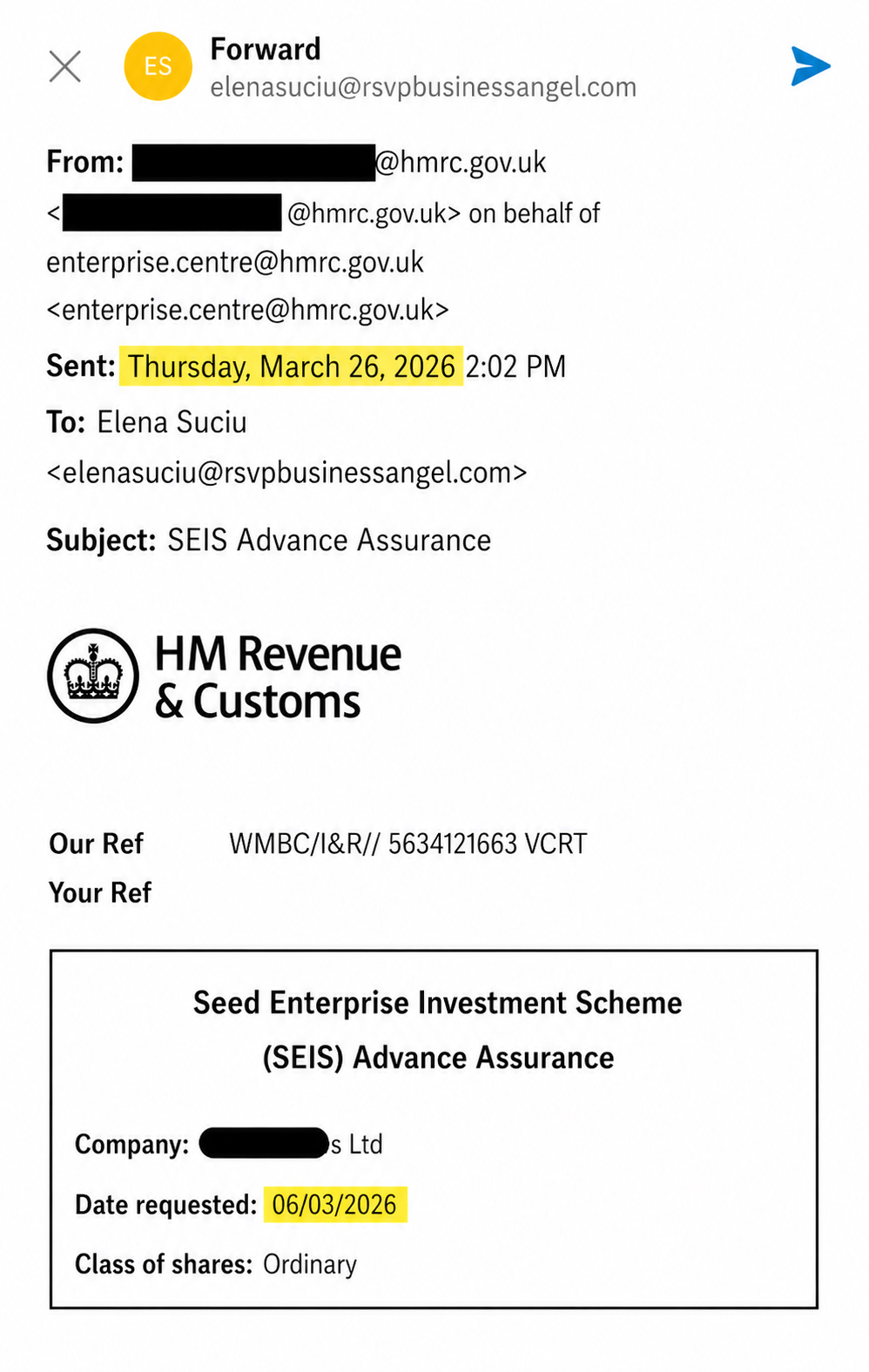

Approved by HMRC in 20 days, on first read.

What was asked of the CFO.

A UK FoodTech venture — proprietary fermentation processes applied to functional ingredients, supplying B2B food manufacturers, not an FMCG brand. The founders had received innovation grant funding and were preparing to raise private capital. They needed SEIS Advance Assurance in place before approaching investors.

The brief was narrow on paper, demanding in execution: take an IP-heavy, partly grant-funded FoodTech venture and align it — without distorting the science — with the SEIS eligibility criteria HMRC actually evaluates against.

Where the SEIS friction actually sat.

The complexity was not in the science. It was in the alignment between a FoodTech venture funded partly by innovation grants and the SEIS evaluative framework.

- 01

Process IP, not product IP.

The defensible asset was the fermentation process and its reproducibility — not a SKU. The submission had to evidence a qualifying trade and risk-to-capital logic without reducing the venture to a product story.

- 02

Grant-funded R&D preceding private capital.

Innovation grants had de-risked the science. SEIS capital had to be positioned as funding genuine commercial growth — manufacturing scale, supply contracts, market entry — and not subsidising activity already covered.

- 03

Cap table and governance instability.

Early-stage shareholder movements had left the ownership structure ambiguous. Before any HMRC narrative could hold, governance and the cap table had to be reset to a clean, investor-credible baseline.

- 04

Risk-to-capital narration.

The application had to read on first pass — to a reviewer with no domain context — as a venture taking genuine commercial risk with the capital it sought, in the precise sense HMRC tests for.

The CFO work, in the order it was done.

- Step 01

Eligibility diagnostic.

Tested the venture against the SEIS company conditions, qualifying trade definitions and the risk-to-capital framework before drafting anything investor-facing.

- Step 02

Cap table & governance reset.

Ownership and decision-making rebased to a clean, investor-credible structure. Pre-empted the questions HMRC and any subsequent investor would otherwise raise.

- Step 03

Three-year financial model.

Built a 3-year operating model ring-fencing grant-funded R&D from the rest of the capital base — SEIS proceeds, founder capital and forecast revenue tracked on separate lines, with use-of-funds, headcount, manufacturing scale-up and breakeven derived from the same source of truth.

- Step 04

Risk-to-capital narration.

Drafted the technical narrative against HMRC's evaluative criteria: genuine commercial risk, growth use-of-funds, no asset preservation, capital that scales the venture rather than entrenches it.

- Step 05

Submission engineered for first read.

Application written so a generalist HMRC reviewer — without FoodTech or fermentation expertise — reaches the right conclusion without needing follow-up correspondence.

HMRC outcome of record.

| SEIS Advance Assurance | Approved |

| Time to decision | 20 days |

| HMRC follow-up queries | 0 |

| Re-submission required | No |

Source: HMRC correspondence on file.

Evidence on file.

Source documents retained from HMRC correspondence. Identifying detail redacted under engagement confidentiality.

Original ref: WMBC/I&R/ 5634121663 VCRT. Date requested: 06/03/2026 — Date approved: 26/03/2026. Class of shares: Ordinary. Company name and HMRC officer identifiers redacted.

On the engagement.

“This is really fantastic — thank you so much for your hard and thoughtful work.”

Client identity withheld under engagement confidentiality. Quote retained on file.

What this case demonstrates.

The fractional-CFO value is not the model. It is the diagnosis, the sequencing, and the narration HMRC reads on first pass.

- →Reading a FoodTech venture against SEIS criteria before drafting investor-facing material.

- →Resolving cap-table and governance friction as a pre-condition for credible HMRC narration.

- →Building a 3-year financial model that ring-fences grant-funded R&D from the rest of the capital base.

- →Engineering the submission so a generalist HMRC reviewer reaches the right conclusion on first read.